All Categories

Featured

Table of Contents

According to SEC officials, existing CDAs have actually been registered as securities with SEC, and therefore are covered by both federal safeties regulations and guidelines, and state insurance policy policies. At the state level, NAIC has developed state disclosure and viability regulations for annuity items. States vary on the level to which they have taken on these annuity guidelines, and some do not have defenses at all.

NAIC and state regulators told GAO that they are presently examining the guidelines of CDAs (3 year fixed annuity). In March 2012, NAIC started evaluating existing annuity laws to identify whether any type of modifications are needed to address the unique item layout features of CDAs, consisting of possible modifications to annuity disclosure and viability standards. It is likewise assessing what kinds of resources and reserving requirements may be needed to help insurance companies take care of product risk

What Is The Best Annuity

Both concur that each state will certainly have to reach its very own final thought concerning whether their certain state guaranty fund laws permit CDA protection. Until these governing problems are dealt with, customers may not be fully safeguarded. As older Americans retire, they might deal with rising healthcare expenses, inflation, and the risk of outlasting their possessions.

Lifetime revenue items can aid older Americans ensure they have income throughout their retirement. VA/GLWBs and CDAs, 2 such items, might supply one-of-a-kind benefits to customers. According to industry participants, while annuities with GLWBs have actually been cost a variety of years, CDAs are reasonably new and are not widely offered.

GAO supplied a draft of this record to NAIC and SEC (government annuities). Both offered technological remarks, which have been dealt with in the record, as proper. For even more information, get in touch with Alicia Puente Cackley at (202) 512-8678 or

It assures a fixed rate of interest rate yearly, no matter of what the securities market or bond market does. Annuity assurances are backed by the monetary strength and claims-paying capability of American Cost savings Life Insurance Business. Defense from market volatility Ensured minimum rates of interest Tax-deferred money build-up Ability to stay clear of probate by assigning a beneficiary Choice to transform component or every one of your annuity into an income stream that you can never outlive (annuitization) Our MYGA uses the ideal of both worlds by ensuring you never shed a cent of your principal financial investment while all at once guaranteeing a rates of interest for the selected time period, and a 3.00% ensured minimum passion price for the life of the agreement.

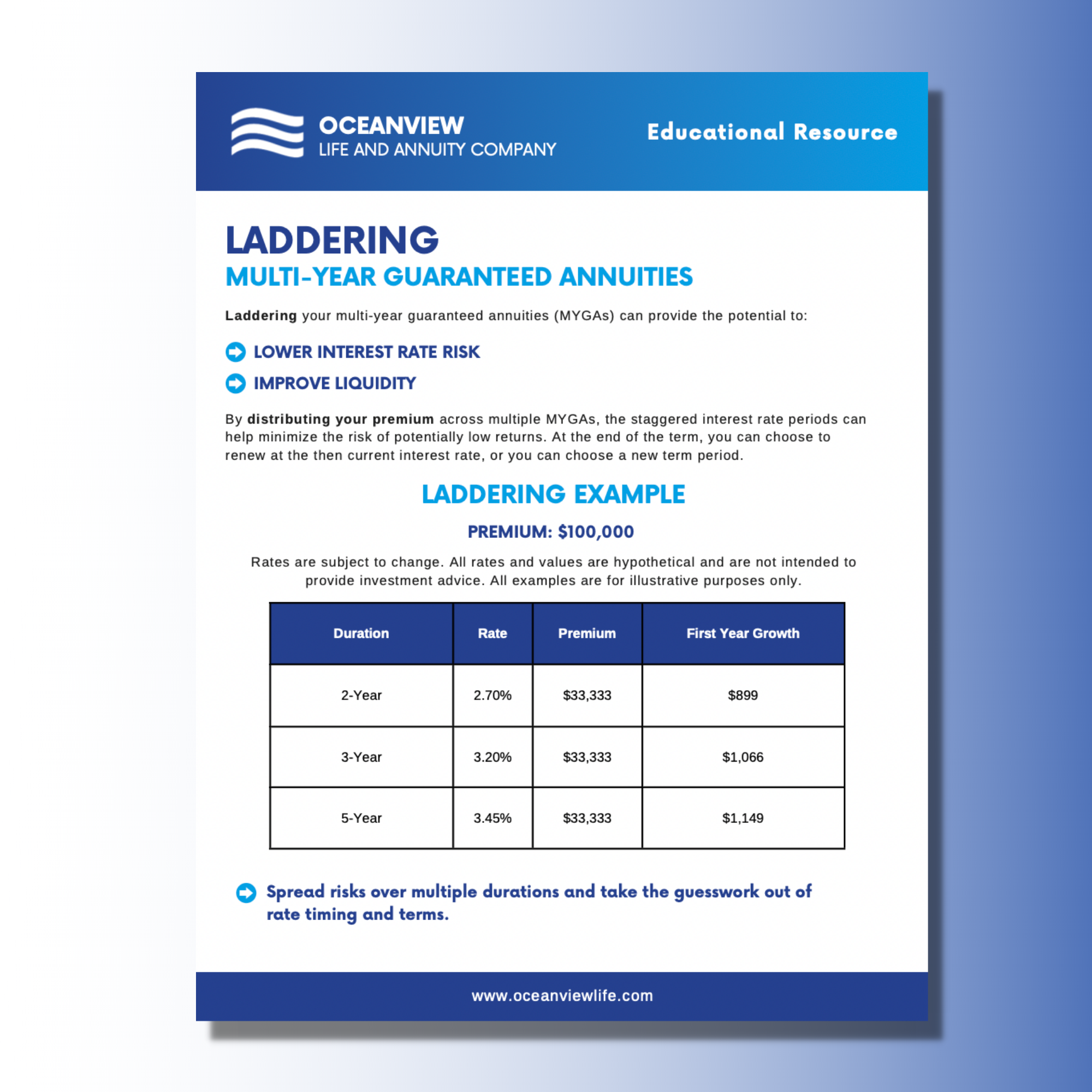

The rate of interest price is guaranteed for those surrender charge years that you choose. We have the ability to pay above-market rate of interest as a result of our below-average expenses and sales costs in addition to our constant above-average monetary performance. 1-Year MYGA 5.00% 2-Year MYGA 5.25% 3-Year MYGA 5.25% 4-Year MYGA 5.25% 5-Year MYGA 5.25% 10% Annual Penalty-Free Withdrawal Rider (no charge) Penalty-Free Survivor benefit Rider (no charge) Penalty-Free Persistent Health Problem Biker (no charge) Penalty-Free Terminal Ailment Rider (no charge) Penalty-Free Nursing Home Confinement Cyclist (no price) Multi-Year Surefire AnnuityAn Individual Solitary Premium Fixed Deferred Annuity Rates Of Interest Options(Interest rates differ by thenumber of years chosen) 1-Year: 1-year surrender charge2-Years: 2-years surrender charge3-Years: 3-years give up charge4-Years: 4-years surrender charge5-Years: 5-years surrender charge Concern Ages 18-95 years old: 1 or 2 years durations18-90 years old: 3, 4, or 5 years durations Concern Age Resolution Current Age/ Last Birthday Minimum Costs $25,000 Maximum Costs $500,000 per individual Price Lock Allocations For situations such as individual retirement account transfers and IRC Section 1035 exchanges, an allocation might be made to lock-in the application day interest rateor pay a greater rates of interest that might be available at the time of concern.

Rates efficient since November 1, 2024, and undergo transform without notification. Withdrawals are subject to common income taxes, and if taken before age 59-1/2 may sustain an additional 10% government charge. Early surrenders might cause invoice of much less than the initial costs. guaranteed retirement income. Neither American Cost Savings Life nor its producers offer tax obligation or lawful recommendations.

Annuity Policy

Loading ... Sorry, a mistake was run into packing the information. Based on the life with money reimbursement option for a plan bought by a male annuitant with $100,000. These payout prices, which include both interest and return principal. The rates represent the annualized payment as percent of overall costs. 4. The New York Life Clear Income Advantage Fixed AnnuityFP Collection, a fixed deferred annuity with a Surefire Life Time Withdrawal Advantage (GLWB) Biker, is provided by New york city Life Insurance Coverage and Annuity Firm (NYLIAC) (A Delaware Corporation), an entirely owned subsidiary of New york city Life Insurance Policy Company, 51 Madison Opportunity, New York City, NY 10010.

All guarantees are reliant upon the claims-paying ability of NYLIAC. There is a yearly cyclist charge of 0.95% of the Accumulation Value that is deducted quarterly. Based on the life with cash money refund option, male annuitant with $100,000.

An assured annuity price (GAR) is a promise by your pension provider to offer you a details annuity rate when you retire.

2 Types Of Annuity

, which can also provide you a better rate than you 'd generally obtain. And your guaranteed annuity may not include functions that are important to you. annuity annuitization.

An ensured annuity rate is the price that you get when you get an ensured annuity from your carrier. This impacts just how much earnings you'll receive from your annuity when you retire. It's great to have an ensured annuity price because maybe much more than existing market prices.

Surefire annuity rates can go as high as 12%. That's approximately double the ideal prices you'll see on the market today.

New York Life Guaranteed Lifetime Income Annuity Ii

If you choose to move to a flexi-access pension, you might need to talk to a financial adviser. There may also be restrictions on when you can establish up your annuity and take your guaranteed price.

It's an information that commonly obtains buried in the fine print. best 2 year fixed annuity rates. Your service provider might call it something like a 'retirement annuity contract', or describe a 'Area 226 policy', or simply discuss 'with-profits', 'advantages', 'special' or 'assure' annuities. So to figure out if you have actually obtained one, the most effective thing to do is to either ask your service provider directly or contact your economic consultant.

An annuity assurance period is extremely different from a guaranteed annuity or assured annuity price. This is a fatality advantage choice that switches your annuity payments to a liked one (normally a companion) for a specific amount of time as much as 30 years - when you pass away. An annuity warranty period will offer you satisfaction, but it likewise indicates that your annuity earnings will be a little smaller.

If you select to transfer to another supplier, you may lose your assured annuity price and the benefits that come with it. Yes - annuities can come with several different kinds of warranty.

Sell My Annuity

That can make points a little complex. As you can envision, it's easy to state a guaranteed annuity or an ensured annuity price, meaning a guaranteed revenue or annuity warranty duration. Ensured annuity prices are in fact very various from them. So when individuals or business start discussing annuity warranties, it is very important to make certain you understand exactly what they're defining.

{kind=link}

Table of Contents

Latest Posts

Breaking Down What Is Variable Annuity Vs Fixed Annuity A Comprehensive Guide to Investment Choices Breaking Down the Basics of Fixed Income Annuity Vs Variable Growth Annuity Features of Fixed Vs Var

Decoding How Investment Plans Work Key Insights on What Is A Variable Annuity Vs A Fixed Annuity What Is the Best Retirement Option? Benefits of Fixed Income Annuity Vs Variable Annuity Why Choosing t

Exploring the Basics of Retirement Options A Comprehensive Guide to Fixed Vs Variable Annuity Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Variable Annuity V

More

Latest Posts